By David B. Mandell, JD, MBA and Jason M. O’Dell, MS, CWM

From our experience, we have become intimately familiar with how most physicians build their financial plans (what we call “wealth plans”). Too often, they have ignored the most important factor in a sophisticated long term plan – flexibility.

Because so much of life doesn’t work out exactly how one plans, it would seem obvious that flexibility should be fundamental to a wealth plan. This is especially so in the financial arena, since many factors that may make the difference between hitting your financial goals or not are beyond your control.

In this 2-part article, we will examine the important factors for which your wealth plan must provide flexibility. Let’s examine the first two here:

1. Changes in Income/Cash Flow

This is likely the most “top of mind” for physicians. With the federal government cutting reimbursements, private insurers following, and inflation still causing overhead costs to rise, this is not surprising. Add to this the increasing numbers of doctors who are becoming employed – where the income will be dictated by a hospital or health system – and this clearly becomes the most important factor where flexibility is required. The plain facts are that most doctors cannot accurately predict their income in future years right now, so flexibility has to be part of the plan.

How do you incorporate income/cash flow flexibility into a wealth plan? Two important factors are to live below your means and make saving each month, quarter and year a priority now. These two elements can combine to position you well to weather any temporary or even long-term hits to income/cash flow.

Another important tactic here is to implement savings vehicles that allow for uneven funding/investments. As an example, in the qualified retirement plan (QRP) arena, this might mean using defined contribution plans that allow flexibility in contributions each year – as opposed to a defined benefit plan which can require a certain level of funding or cause underfunding penalties. Even more relevant would be to utilize “hybrid” or fringe benefit plans that may allow much higher contributions than defined contribution plans when income is high but can actually be skipped entirely in years where income wanes.

Another example here would be in the asset class of permanent life insurance – one that has the benefit of tax-deferred growth and top asset protection in many states. Here, funding flexibility would favor a “universal life” type policy — where, as above, funding is flexible year-to-year — over a “whole life” type policy, where funding must occur each year.

2. Changes in Tax Rates

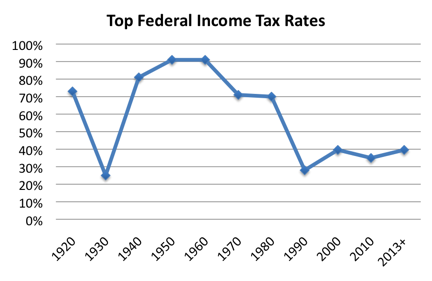

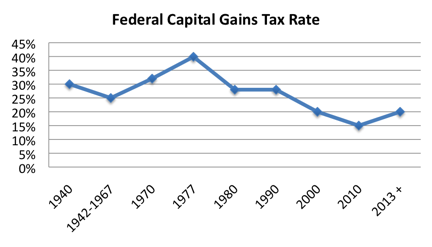

Right behind the #1 factor of cash flow/income, the #2 planning element that one should build flexibility around is taxes. As of the beginning of 2012, we are at the 3rd lowest federal income tax regime (measure by the highest bracket) since the income tax was implemented nearly 100 years ago and the very lowest capital gains tax rates since the 1940s when that tax was enacted. See charts below, which show the top marginal federal income tax rate and federal capital gains tax rate in effect for each decade on the “0 year” (i.e., 1920, 1930, 1940, 1950, etc.). These charts do not show state income or capital gains rates.

Examining these charts, it seems quite apparent that we could see tax rates rise. If they even return to mean rates of the 20th century, we will experience a sharp increase in tax rates. Thus, it makes sense to build in flexibility for this possibility.

In our firm, we approach this through a process of “tax diversification.” While most firms focus only on asset class diversification in the context of investing, we believe it is crucial to layer on top of this focus a concentration to diversify a client’s wealth to tax rate exposure.

As an example, we might look at a client’s QRP assets as those that are subject to future income tax increases – since, to get access to QRP funds; you have to pay ordinary income taxes. Further, most personally-owned assets are subject to future capital gains tax increases – from securities to real estate to closely held business interests to commodities or artwork. As capital gains tax rates increase, the value of these assets decline – at least in terms of how they might assist you in retirement.

Applying a “diversification” approach, we find that most physicians are inadequately invested in asset classes or structures that are immune to future income or capital gains tax increases. Whether these options are in the form of cash value life insurance, tax-free municipal bonds, ROTH IRAs or others, they should be part of every doctor’s wealth plan. Bottom line: you need to have flexibility against the possibility that tax rates increase, especially if those increases are significant.

Applying a “diversification” approach, we find that most physicians are inadequately invested in asset classes or structures that are immune to future income or capital gains tax increases. Whether these options are in the form of cash value life insurance, tax-free municipal bonds, ROTH IRAs or others, they should be part of every doctor’s wealth plan. Bottom line: you need to have flexibility against the possibility that tax rates increase, especially if those increases are significant.

Conclusion

Because risk and uncertainty are so prevalent over the long term, flexibility is a crucial element of a conservative, yet creative, wealth plan. In this article, we looked at 2 key elements around which any plan should build flexibility – changes in income and in tax rates. In part II of the article, we will examine 3 additional elements – changes in the “market,” in liability, and in health.

###

David Mandell, JD, MBA, is an attorney, author of five books for doctors, and principal of the financial consulting firm OJM Group. Jason M. O’Dell, MS, CWM is also an author of multiple books for physicians and a principal of OJM Group. They can be reached at 877-656-4362. This article contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized legal or tax advice. You should seek professional tax and legal advice before implementing any strategy discussed herein.